OBR turns a blind eye to Net Zero policy risks

The Office for Budget Responsibility (OBR) has failed to assess the true risks of the government's Net Zero policy and is not a reliable guide to the long-term sustainability of Britain's public finances.

The latest Fiscal Risks Report from the UK government’s independent Office for Budget Responsibility (OBR) devotes much of its discussion to the costs of implementing the 2050 Net Zero emissions target. Unfortunately, it has failed adequately to discharge its statutory duty to analyse the true risks this policy poses to the sustainability of the public finances. While it correctly notes a significant potential impact from the 'indirect effects' of climate policies it has failed to assess the possibility that these indirect effects could be significantly negative, causing economic contraction that reduces both income and corporation tax receipts.

In short, the OBR’s Fiscal Risks Report 2021 has failed to produce a credible risk assessment and is not a reliable guide to the long-term sustainability of the public finances.

This defect flows from the fact that the OBR relies all but exclusively on the opaque and tendentious cost estimates of the Climate Change Committee (CCC), which are extremely optimistic about the net cost of low carbon policies and thus project correspondingly unrealistic technology deployment scenarios. In sharp contrast to its excessive optimism about Net Zero, the OBR presents an unbalanced emphasis on pessimistic assessments of the costs of climate change.

Unjustified optimism on the one hand, and blinkered pessimism on the other results in an overall lack of balance that means the resulting fiscal risk assessment is both incomplete, distorted and unfit for purpose.

A wider range of scenarios, from a wider range of sources, with a stronger emphasis on current trends, however discouraging, not wishful thinking about the future, is badly needed.

This inadequate report is yet more evidence that the lack of objectivity in the institutions of British government has itself become a fiscal risk factor, jeopardising the state’s reputation and potentially increasing the cost of public borrowing, as well as making the UK a less attractive jurisdiction in which to invest capital.

Analysis

The UK government’s independent Office for Budget Responsibility (OBR) has in the last week published its latest Fiscal Risks Report. It devotes a large part of the document (pages 83–152) to the consideration of climate change policies, concluding that the “Between now and 2050, the fiscal costs of reducing net emissions to zero in the UK could be significant but not exceptional” (p. 150).

It is important to recall that this conclusion is narrowly focused on fiscal implications. The OBR does not consider the wisdom of current policies overall for British citizens, but only the implications of those policies for the public finances.

The Office for Budget Responsibility operates under a remit set out in the Budget Responsibility and National Audit Act (2011) which states that the OBR has the duty of examining and reporting on “the sustainability of the public finances” (see paragraph 4(1)), with the specific obligation to reveal in its reports all the assumptions it has made as well as giving an account of “the main risks which the Office considered to be relevant” (6(b)).

Though narrow, this is not an undemanding specification, and it is reasonable to ask whether the OBR has adequately discharged its statutory duties in this latest report. There are good grounds for thinking it has not done so.

On page 123 the OBR authors write, correctly, that “An assessment of the fiscal risks posed by the transition to net zero must take account of four different ways in which this transition can affect the public finances”. The four items are listed as follows:

First, government is likely to be called upon to bear some of the direct cost of transition described above, at the very least for the buildings it occupies and vehicles it operates.

Second, it faces a direct loss of tax revenues linked to fossil fuels and emissions.

Third, it could derive a direct revenue benefit by taxing carbon more heavily.

Fourth, it must contend with the indirect effects (which could be negative or positive) of the transition on the public finances via wider economic outcomes.

Of these four fiscal risks, the OBR, remarkably, only analyses the first three in detail, ignoring close assessment of the fourth risk.

The credibility of the assessment of these matters is further undermined by the fact that it is all but exclusively reliant on the Climate Change Committee (CCC) for its estimates on policy costs and technology deployment rates, though reference is also made to equally optimistic economic growth scenarios from the Bank of England (summarised in 3.26, which shows a complete return to trend after the pandemic by 2023-2024, and an economy in 2050 almost 1.6 times larger than it is at present).

It is bad enough that this blinkered optimism undermines confidence in the OBR’s projections of direct fiscal costs to government, but the danger of mistakes concerning indirect effects is of even greater magnitude and suggests that the OBR has neglected the main risks it has identified as relevant, failing to discharge its statutory duties.

The fragility and opacity of the Climate Change Committee’s assumptions, for example concerning the costs of offshore wind, are well known. The OBR did not take into account the likelihood that the “indirect effect” it has identified as a fiscal risk is significantly negative and that the Net Zero costs could be much higher than its already startling £1.4 trillion cost estimate. It did not consider the risk that far from seeing steady upwards growth, the UK economy might stagnate or even contract as scarce resources were transferred on a large scale into low productivity energy sources (wind, solar) and high cost conversion devices (heat pumps, Electric/Hydrogen Vehicles), thus increasing production costs, eroding UK competitiveness and reducing fiscal receipts from income and corporation tax.

That the OBR did not exercise this elementary caution is inexplicable. All the data required to start the alarm bells ringing can be found in its own pages. Table 3.1 in the study, for example, describes the three CCC Net Zero scenarios, which are implicitly presented as the Pessimistic (“Headwinds”) Optimistic (“Tailwinds”) and Middle ground (“Balanced”) pathways.

But a glance at the table shows that even “Headwinds” is highly optimistic, projecting 75% of electricity from renewables, Electric Vehicles as forming 100% of sales in 2035, and over 70% of households using hydrogen for heating.

The “Balanced” and “Tailwinds” scenarios are still more extreme, the latter projecting 90% renewable electricity, a 50% reduction in meat and dairy consumption, the planting of 70,000 hectares a year by 2035, and a 15% per cent reduction in flying.

Transformational change on this scale is obviously an extremely a high-risk undertaking, with physical, economic, and political dangers - but the OBR does not consider any alternative to the CCC’s view that this will undoubtedly be economically beneficial and politically acceptable to the United Kingdom.

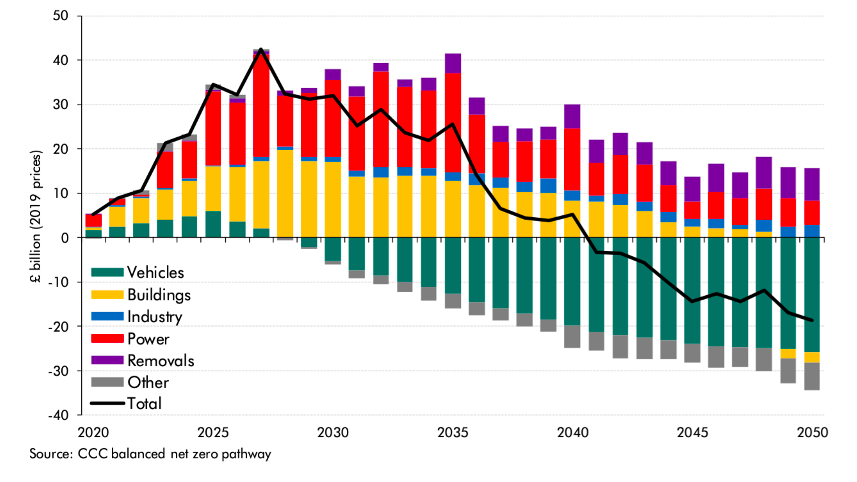

The scale of this gamble can be clearly seen in the OBR’s use of the CCC’s predictions for the net cost by sector of reaching Net Zero via the “Balanced” pathway:

Net cost by sector of reaching net zero in the CCC’s balanced pathway. Figure 3.12 in the OBR, Fiscal Risk Report 2021, p. 107.

The black line on the chart represents the total net cost to the economy expected by the CCC, and starts to fall by 2027, delivering a major saving from 2040 onwards.

But that net saving is critically dependent on reductions in the cost of transport in spite of a shift to electricity and hydrogen. The OBR reports that these technologies will deliver “operating savings” of £30 billion a year in 2050 (p. 108), justifying this claim by reporting that “over the next decade, battery prices are projected to fall rapidly”, with “running costs” becoming cheaper than petrol and diesel as early as 2025.

The cause of this incredible fall in running costs must be attributed primarily to the assumption of low cost renewable electricity (see p. 119), but also to the imposition of a carbon tax on fossil transport fuels. The OBR assumes that consumers will quietly accept a carbon tax of £101 per tonne of carbon dioxide in 2026, roughly double the Social Cost of Carbon, and five times the UK Emission Trading Scheme (UKETS) price, rising to over £180 a tonne in 2050.

In fact, most of the projected saving is due not to a decline in battery costs but to these dramatic assumptions about cheap electricity and the imposition of carbon taxation, a point that can be clearly seen in the OBR’s own chart of the detailed effect, drawn once again from the Climate Change Committee:

Surface Transport: Whole Economy Net Costs. Figure 3.14 in OBR, Fiscal Risk Report (July 2021), 110. Source: CCC balanced net zero pathway.

Note that the annual investment costs (capex) on cars and vans hardly falls at all over the period 2025 to 2050 and is predicted to be rising at the end of that period. The net cost reduction predicted in the black line is being delivered by “operating savings”, in other words low-cost renewable electricity and hydrogen.

It is no exaggeration to say that everything in both the CCC’s and the OBR’s cost assessment depends on their optimistic assumption that the cost of renewable electricity will drop significantly. Given that sensitivity, the OBR should at the very least have considered the possibility that the reductions in renewable electricity costs claimed to be likely in the mid 2020s would not materialise. A number of analysts have been warning that in the light of empirical data in company reports this downbeat scenario is more likely than not.[1]

Caution on the underlying trends in capital cost and operating cost for offshore wind are by no means unknown to the financial markets. No one will be surprised that the Climate Change Committee has simply ignored these concerns in its zeal to make the case for Net Zero, but the OBR, with its statutory duties towards the public finances, has no excuse for failing to assess these significant policy risks which have been known for some time now.

Indeed, this latest Fiscal Risks Report confirms general concerns that the topic of climate change has induced a general institutional failure of responsibility in the British government. There is a growing tendency to unquestioningly copy and paste optimistic assessments about policy costs and risks from one report to another. The taxpayers who pay the salaries of these civil servants will look in vain for independent critical thinking, for the operation of the checks and balances which should prevent group-think and systemic policy error.

There is a real possibility, and we would say a high likelihood, that the Climate Change Committee is mistaken about the costs of the Net Zero transition, and that indirect economic effects, correctly identified but not adequately examined by the OBR, will be severely negative for the economy as a whole and the public finances, with stuttering economic activity and stagnant or even falling tax receipts.

One might even say that the absence of cool-headed and credible analysis within government is now itself becoming a fiscal risk factor of significance. International financial analysts and investors will undoubtedly see the OBR's excessive optimism for what it is, a political exercise, a policy delivery boost, not the unbiased and comprehensive risk analysis and sanity-check that one expects from a competent administration. Over-optimism and the absence of rigorous internal scrutiny can only undermine the credibility of the British state, with poisonous implications for the cost of government borrowing and for the prospects for inward investment. Britain is beginning to look like a text-book example of a failing planned economy.

Note

[1] For empirical data and analysis of offshore wind energy costs see